Navigating the market's uncertainties requires intuition and strategy and a solid foundation in risk management. It's essential for traders to have a method to assess potential losses, preparing them for the inherent volatilities of the financial world. This is where Crypto Valley Exchange steps in, adopting the Value-at-Risk (VaR) model as a sophisticated tool for risk evaluation. The VaR model is a testament to CVEX's commitment to providing its users with advanced resources to manage risk effectively. Let's delve into the principles of the VaR model and how it transforms risk assessment on CVEX.

The Value-at-Risk model stands out as a statistical measure designed to estimate the potential loss in the value of a portfolio over a defined period for a set confidence interval. VaR calculates the maximum expected loss under normal market conditions, offering traders a clear perspective on the risk associated with their positions. This ability to quantify financial risk within a specific timeframe is invaluable. It enables traders to gauge the extent of potential losses and adjust their strategies accordingly, fostering a more informed and cautious approach to trading. Through adopting the VaR model, CVEX empowers its traders with a quantifiable risk assessment, setting a new standard in the careful navigation of the financial markets.

Efficient Capital Usage. The VaR model aligns margin requirements with actual risk exposure, reducing the need for excessive capital allocation towards margins. This allows traders to utilise their capital more effectively, enabling additional trading activities and enhancing portfolio diversification.

Dynamic Risk Assessment. Adapting to market changes and volatility, the VaR model ensures that margin requirements are always reflective of current market conditions. This adaptability helps traders stay prepared for fluctuations without the burden of unnecessary margins.

Enhanced Trading Safety and Stability. By providing a realistic measure of potential losses, the VaR model helps traders make informed decisions, significantly reducing the likelihood of unexpected losses. This contributes to a more secure and stable trading environment on CVEX.

At the heart of CVEX’s adoption of the Value-at-Risk model lies a sophisticated calculation methodology, meticulously carried out by Risk Oracles. Unlike the traditional historical method, which relies heavily on past return values and can be skewed by extreme market events, CVEX embraces a statistical approach. This methodology ensures a more balanced and comprehensive risk assessment by considering the full range of available data.

The process begins with the Risk Oracles assessing the historical prices of assets, converting these into log returns, and normalising them to eliminate bias. This preparation is crucial for accurately fitting the data into a statistical distribution model, moving away from the potential pitfalls of the historical method's sensitivity to tail values.

By utilising the entire data spectrum, the statistical method allows for a precise evaluation of potential losses, accounting for the complexities and nuances of market behavior. This approach not only mitigates the irregularities associated with extreme market conditions but also provides a more reliable foundation for calculating margin requirements.

In transitioning from the historical to a statistical methodology, CVEX ensures that its VaR model remains robust, responsive, and reflective of the true risk landscape. It's a testament to the platform's commitment to offering traders a reliable, nuanced, and scientifically grounded risk management tool.

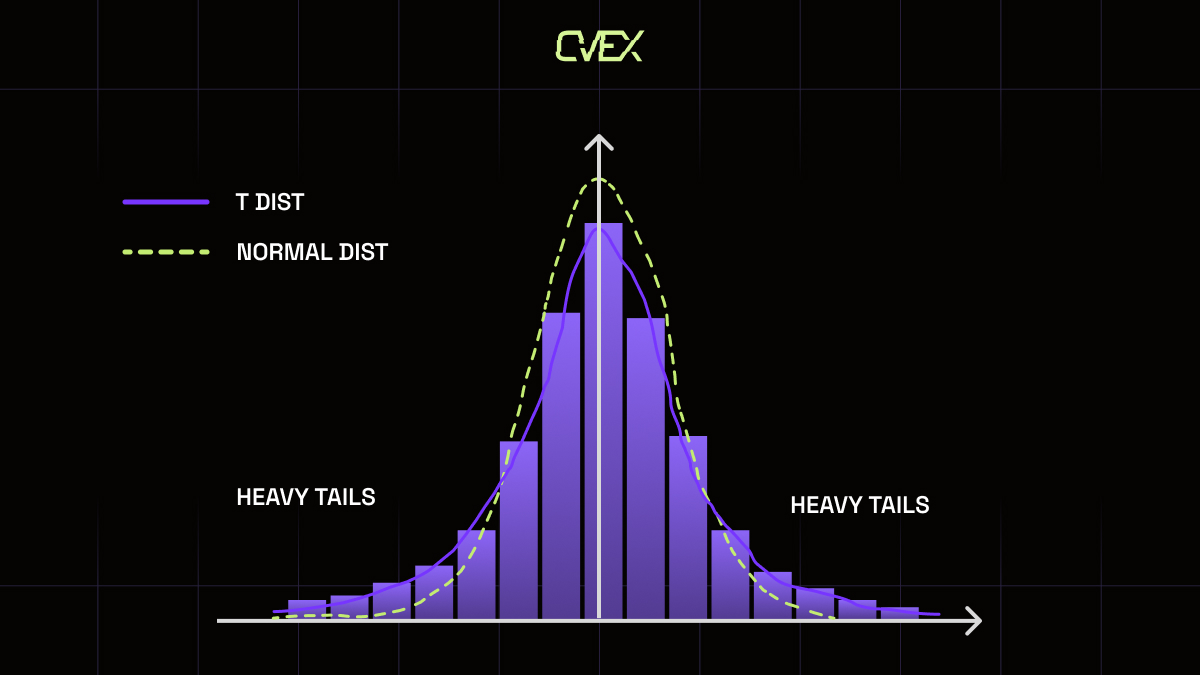

Choosing the Right Distribution for Accurate VaR Results

Accurate VaR calculation hinges on selecting an appropriate distribution model that mirrors market realities, including the 'fat tails' characteristic of market return distributions. The t-distribution emerges as the superior choice over the normal distribution for several reasons:

Understanding and applying the VaR model significantly alters how traders approach risk management and decision-making:

The integration of the Value-at-Risk model into CVEX's trading platform represents a significant advancement in risk assessment for traders. By adopting a statistical approach grounded in the t-distribution, CVEX offers a nuanced and realistic evaluation of potential market risks. This model enables traders to understand their risk exposure better and to make trading decisions that are informed by a comprehensive risk assessment framework. The ultimate benefit of employing the VaR model on CVEX is the empowerment it provides traders, allowing for strategic decision-making bolstered by precise risk analysis. This enhances not just individual trading outcomes but also contributes to the overall stability and safety of the trading environment on CVEX.